July 2025: A Turning Point in AI Sovereignty, Quantum Tech, and Geopolitics.

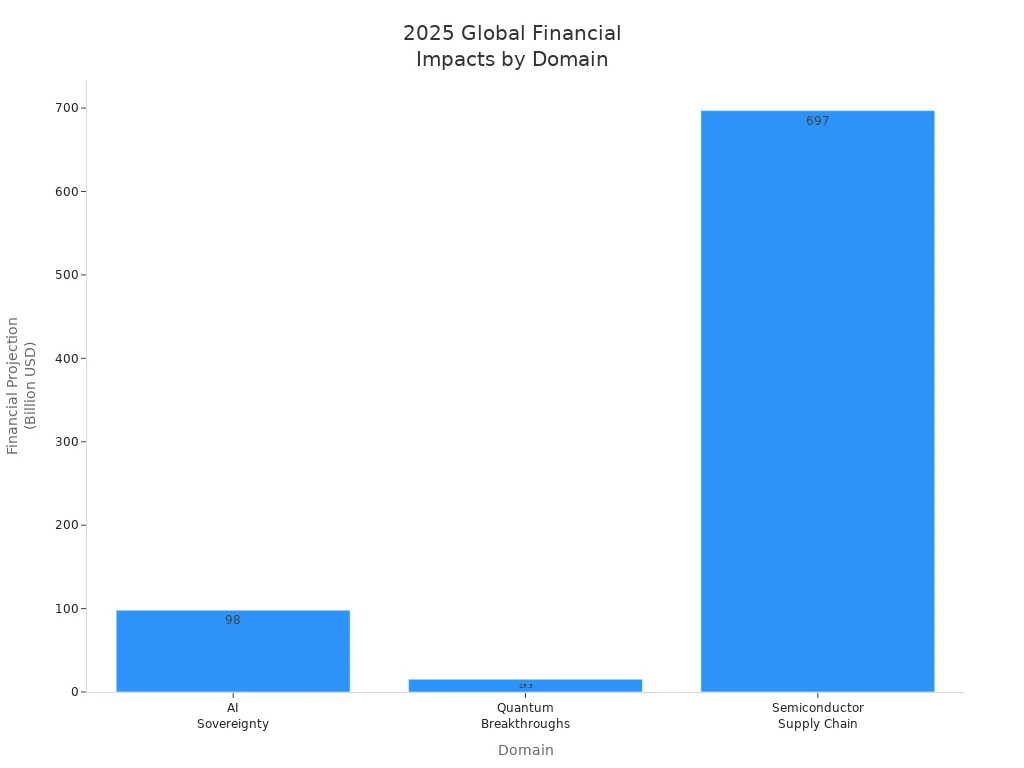

A perfect storm now shapes the global technology landscape. In July 2025, AI sovereignty, quantum breakthroughs, and supply chain shifts collide, creating a unique turning point. The IMF highlights slower global growth and rising tariffs, while the New York Fed points to deep economic uncertainty. Companies and governments face trillion-dollar stakes in AI, quantum, and chips.

The July 2025 inflection will force every leader to rethink strategy, ethics, and operations.

Key Takeaways

July 2025 marks a major turning point as AI control, quantum computing, and chip supply challenges reshape global technology and power.

Countries compete to build their own AI systems and data control, which affects security and economic strength worldwide.

Quantum computing moves from labs to real-world use, helping industries like medicine and defense solve complex problems faster.

Chip shortages and supply chain issues force nations and companies to invest in local production and diversify suppliers.

New laws push companies to be greener, support repairs, and manage e-waste, making sustainability a key business priority.

July 2025 Inflection: The New Tech Power Struggle

The July 2025 inflection marks a new era in the global technology landscape. Three forces—AI sovereignty, quantum breakthroughs, and the semiconductor crisis—are converging to reshape power structures and business strategies worldwide. This section explores what is happening in each area and how these changes define the current tech power struggle.

AI Sovereignty

AI sovereignty has become a central issue for governments and companies. Countries now compete to control their own AI technology stacks, data, and talent. The rivalry between the United States and China has turned into a strategic contest for AI supremacy. This contest shapes national security, economic policies, and international relations.

AI sovereignty means domestic control over data, computing power, skilled workers, and energy for AI development.

The US, China, India, Japan, and Canada are all accelerating efforts to build strong AI sovereignty.

This trend risks creating an AI arms race focused on national security, which may limit the development of AI tools for the public good.

The push for sovereign AI reflects a global shift toward national control over technology.

Example | Description | Actors Involved | Timeframe |

|---|---|---|---|

US boosts domestic chip manufacturing to reduce supply chain risks | US government | 2023-2024 | |

Export restrictions on GPUs to China | US limits export of powerful GPUs to China | US government | 2023-2024 |

Geopolitical AI partnerships | US tech firms partner with Middle East and Europe for sovereign AI | US tech companies, Middle East, Europe | 2024 |

Global sovereign AI strategies | Major powers pursue their own AI policies | EU, South Korea, India, Japan, Canada | 2023-2024 |

The European Union has taken a leading role by enacting the EU AI Act, a comprehensive legal framework with strict risk-based rules and enforcement. The EU also launched InvestAI, mobilizing €200 billion for AI investment, including €20 billion for AI gigafactories. The US, in contrast, uses a fragmented approach with sector-specific rules and state-level bills. China has built its own AI infrastructure behind the "Great Firewall 3.0," requiring all domestic AI training to use local chips.

Countries are choosing AI stacks like they once chose nuclear allies. The July 2025 inflection is setting new digital borders and alliances.

Quantum Breakthroughs

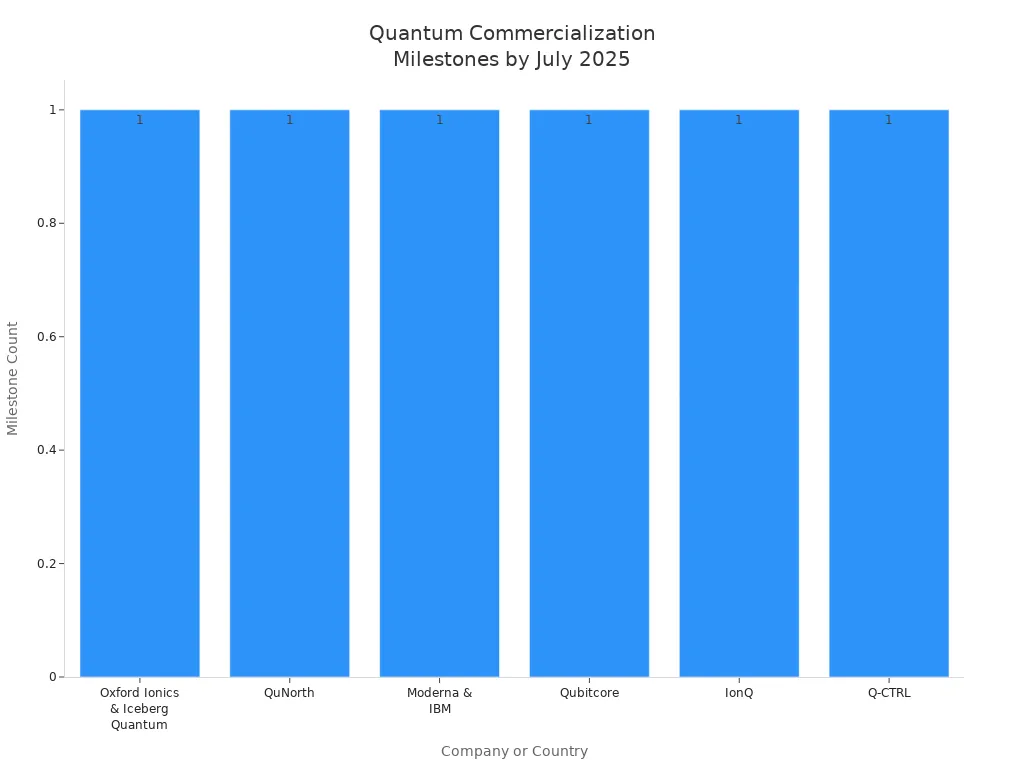

Quantum computing has reached a turning point at the July 2025 inflection. Major companies and countries have announced breakthroughs that move quantum technology from the lab to real-world use.

Companies like Google, Microsoft, and IBM have demonstrated logical qubits with lower error rates, making quantum computers more reliable.

Specialized quantum hardware and software now solve specific problems, such as drug discovery and logistics.

Quantum networking has advanced, with distributed entanglement and city-to-city quantum links.

New types of qubits, such as hole spin and topological qubits, are being tested for better performance.

Several commercialization milestones stand out:

Company/Country | Milestone Description | Date | Impact/Significance |

|---|---|---|---|

Oxford Ionics & Iceberg Quantum (Australia/USA) | Partnership to design fault-tolerant quantum architecture using trapped-ion tech and qLDPC codes. | July 17, 2025 | Advances scalable, error-corrected quantum computing systems. |

QuNorth (Denmark) | €80 million investment to acquire 50-logical-qubit Magne Quantum Computer. | July 17, 2025 | Positions Europe as a key player in commercial quantum computing. |

Moderna & IBM (USA) | Quantum-classical hybrid approach for mRNA research. | July 18, 2025 | Accelerates drug discovery and vaccine development. |

Qubitcore (Japan) | Funding to advance ion-trap quantum computers with distributed architecture. | July 16, 2025 | Breakthrough toward scalable distributed quantum computing. |

IonQ (USA) | Ongoing commercial quantum computing operations. | July 16, 2025 | Demonstrates active market presence. |

Q-CTRL (Australia) | Maritime quantum navigation trials with Australian Defence. | July 16, 2025 | Validates quantum sensing for navigation in defense. |

Quantum breakthroughs are not limited to the US and China. Europe, Japan, and Australia are also making rapid progress. These advances are changing what is possible in fields like medicine, logistics, and defense.

Semiconductor Crisis

The semiconductor crisis is another defining feature of the July 2025 inflection. The world faces ongoing chip shortages, rising prices, and supply chain disruptions.

Demand for chips has surged due to 5G, electric vehicles, and AI.

Supply chain disruptions from the COVID-19 pandemic, natural disasters, and geopolitical tensions have slowed production.

Most advanced chips are made in a few places, like Taiwan and South Korea, making the supply chain fragile.

Long investment cycles mean new factories take years to build.

A 6.4-magnitude earthquake in Taiwan halted production at TSMC, causing delays and losses. China’s export bans on critical raw materials, such as antimony, have led to shortages and price spikes. The US relies heavily on imports of these minerals, increasing its risk. Export controls on advanced manufacturing equipment have limited China’s ability to produce cutting-edge chips.

Semiconductors are now as important to national security as oil or nuclear weapons. Control over chip technology defines superpower status.

Countries are responding by investing in domestic chip production, forming new alliances, and diversifying supply chains. The US, EU, and Japan are all building new fabs and securing raw materials. Companies must adapt by building flexible sourcing and risk management strategies.

The July 2025 inflection is forcing every nation and business to rethink their place in the global tech order. The convergence of AI sovereignty, quantum breakthroughs, and the semiconductor crisis is creating new winners and losers. Those who adapt quickly will shape the future of technology and power.

Sustainability and Regulation

Green Tech Mandates

In 2025, new regulations set clear expectations for technology companies. California SB-253, known as the Climate Corporate Data Accountability Act, requires companies with over $1 billion in annual revenue to disclose greenhouse gas emissions. Annual reports must be submitted to the California Air Resources Board starting in 2025. Scope 1 and 2 emissions reporting begins in 2026, while Scope 3 emissions phase in from 2027. SB-261 adds climate risk disclosures for businesses with revenues over $500 million. These laws create a new standard for transparency.

Leading companies now treat sustainability as a core business priority. Firms like eSparkBiz, Affirma Consulting, and Teravision Technologies deliver eco-friendly digital solutions and comply with environmental standards such as ISO 14001. Their projects show measurable results in emissions reduction and climate risk reporting.

Sustainability is no longer a public relations effort. It shapes research, development, and long-term business value.

Right-to-Repair Laws

Right-to-repair laws have expanded across the United States and Europe. These laws require manufacturers to provide parts, tools, and documentation for repairs. The table below highlights key measures:

Year | Jurisdiction | Law/Measure | Key Provisions and Impact |

|---|---|---|---|

2023 | New York, USA | Digital Fair Repair Act | OEMs must provide repair resources for digital electronics. |

2023 | California, USA | Right to Repair Act | Covers electronics and appliances; model for future laws. |

2024 | European Union | Right-to-repair rules adopted | Makes repairs easier and more cost-effective; pending full adoption. |

2025 | Oregon, USA | Ban on parts pairing | Prevents manufacturers from blocking replacement parts. |

These laws push manufacturers toward greater transparency and support for repair, even as some companies resist.

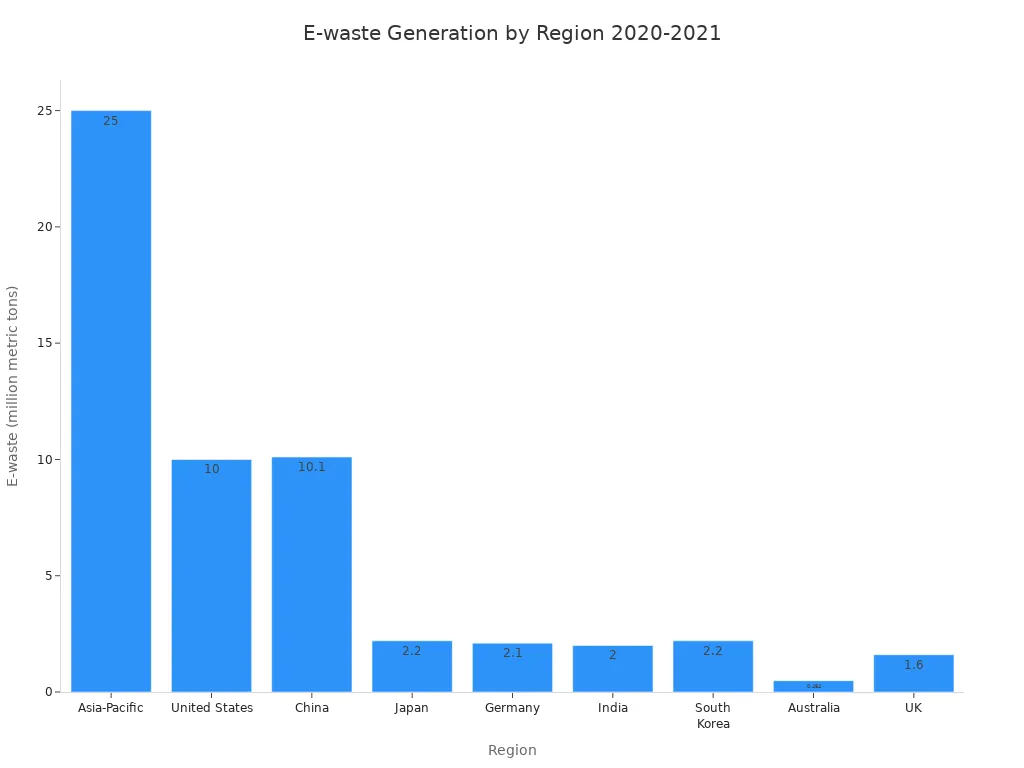

E-Waste and Energy

E-waste continues to rise worldwide. From 2023 to 2025, global annual e-waste generation reaches about 50 million tonnes. Recycling rates remain low, with only 17.4% officially recycled in 2021. The chart below shows e-waste generation by region:

Energy regulations also impact the tech sector. Several countries, including Russia, China, and Canada, have imposed bans or restrictions on Bitcoin mining to protect energy grids. These actions reduce mining activity and increase compliance costs.

Sustainability initiatives now guide research and development. Companies embed decarbonization and resource efficiency into their strategies. AI helps track emissions and improve energy use, but also increases demand for clean power. Sustainability shapes the future of technology innovation and operations.

Workforce and Automation Trends

Tech Talent Shortage

The technology sector in 2025 faces a severe shortage of skilled workers. Companies need experts in AI, quantum computing, and cloud technologies. The global market for quantum computing is expected to reach over $22 billion by 2032. However, the number of qualified professionals remains low. There are 4.2 million unfilled AI positions worldwide, but fewer than 320,000 candidates meet the requirements. Over half of IT leaders report that finding AI talent is now twice as hard as it was two years ago. The average time to fill an AI job is 142 days. This shortage affects industries from healthcare to manufacturing, causing project delays and higher costs.

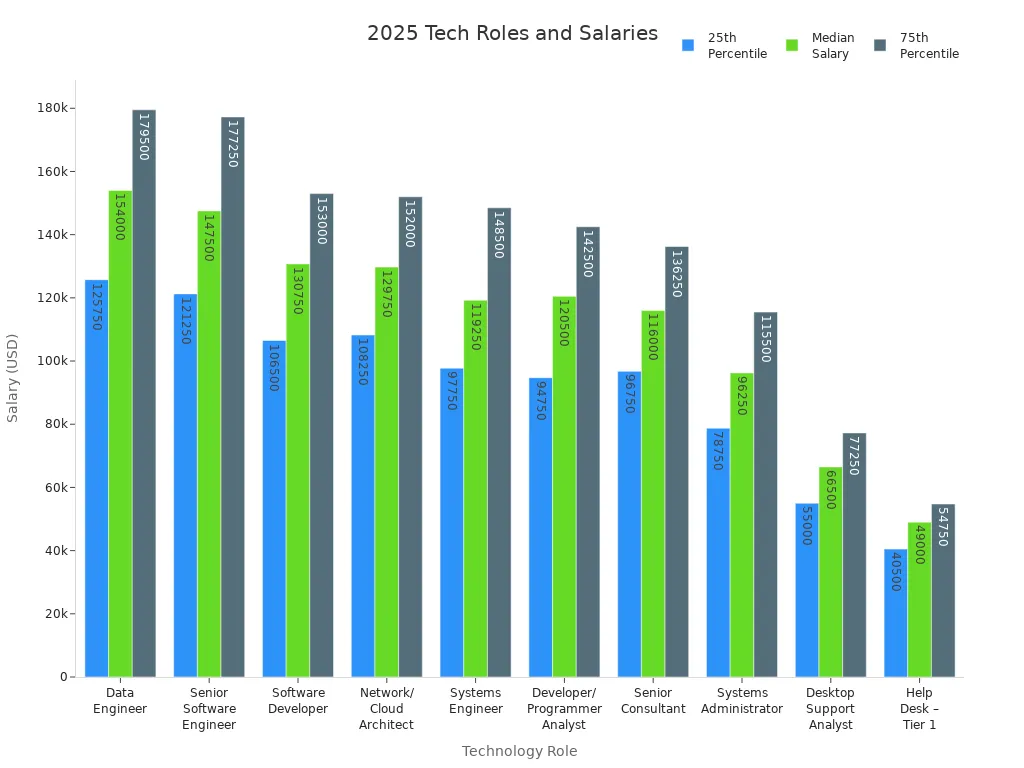

Technology Role | 25th Percentile Salary | Median Salary | 75th Percentile Salary |

|---|---|---|---|

Data Engineer | $125,750 | $154,000 | $179,500 |

Senior Software Engineer | $121,250 | $147,500 | $177,250 |

Software Developer | $106,500 | $130,750 | $153,000 |

Network/Cloud Architect | $108,250 | $129,750 | $152,000 |

AI-Augmented Work

AI tools now help workers complete tasks faster and more accurately. Many companies report a 20-30% boost in productivity from AI-assisted coding. Most executives prefer to hire employees who understand AI. While some jobs have disappeared, most companies use AI to support workers rather than replace them. About 14% of workers have lost jobs due to automation, but many new roles have appeared, such as AI trainers and governance professionals. Workers say AI improves job performance and work-life balance. Companies focus on upskilling their teams to keep up with new technology.

Skills and Education

Technology skills change quickly. The average skill becomes outdated in less than five years. Bootcamps and universities update their programs often to match industry needs. Bootcamps offer hands-on learning and flexible schedules, making it easier for people to gain new skills. Universities now partner with tech companies and bootcamps to provide hybrid courses and stackable credentials. Students learn both technical and soft skills, preparing them for jobs in AI and quantum computing. Schools also face new challenges, such as keeping student data safe and teaching ethical use of AI. Continuous learning has become essential for anyone working in technology.

The July 2025 inflection brings together technology, policy, and market changes that will shape the next decade. Organizations can respond by:

Mapping supply chain risks and using dual-sourcing to build resilience.

Planning for quantum migration with clear roadmaps and ongoing training.

Embedding ethicists in development teams to guide responsible innovation.

Making sustainability a core part of business and research.

Staying informed and using proven frameworks helps leaders adapt as technology continues to evolve.

FAQ

What is AI sovereignty and why does it matter in 2025?

AI sovereignty means a country controls its own AI systems, data, and technology. In 2025, this control shapes national security, economic growth, and global influence. Countries now build their own AI stacks to protect interests and compete globally.

What makes July 2025 a turning point for quantum computing?

July 2025 marks the first time companies use quantum computers for real-world tasks. Banks, drug companies, and defense agencies now rely on quantum breakthroughs. This shift changes how industries solve problems and protect sensitive data.

What is the semiconductor crisis and how does it affect technology?

The semiconductor crisis refers to ongoing chip shortages and supply chain disruptions. These shortages slow down production of electronics, cars, and AI systems. Companies must find new suppliers and invest in local manufacturing to stay competitive.

What new regulations impact technology companies in 2025?

New laws require companies to report carbon emissions, support right-to-repair, and manage e-waste. These regulations push firms to adopt greener practices and improve transparency. Compliance now affects business reputation and market access.

What skills do workers need to succeed in the 2025 tech landscape?

Workers need skills in AI, quantum computing, and cybersecurity. Companies value hands-on experience and continuous learning. Bootcamps, online courses, and hybrid programs help workers stay current and adapt to rapid changes in technology.

See Also

Key FinTech Challenges: AI Risks, Quantum Threats, And CBDC Turning Points

How AI Consolidations Will Shape Web3 And Tech Sectors In 2025